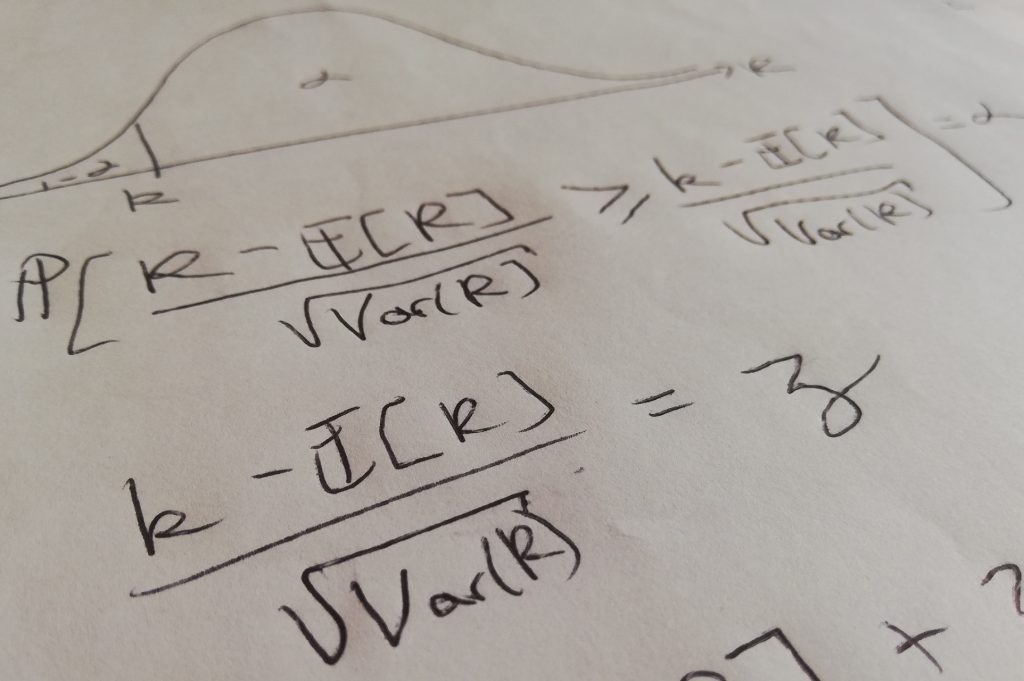

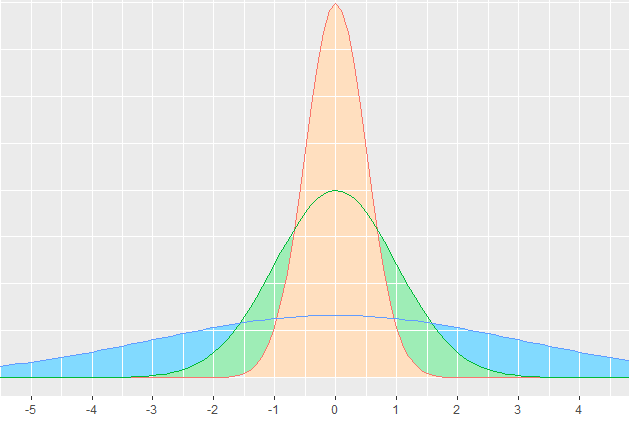

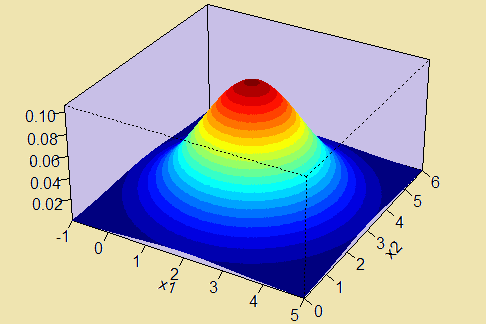

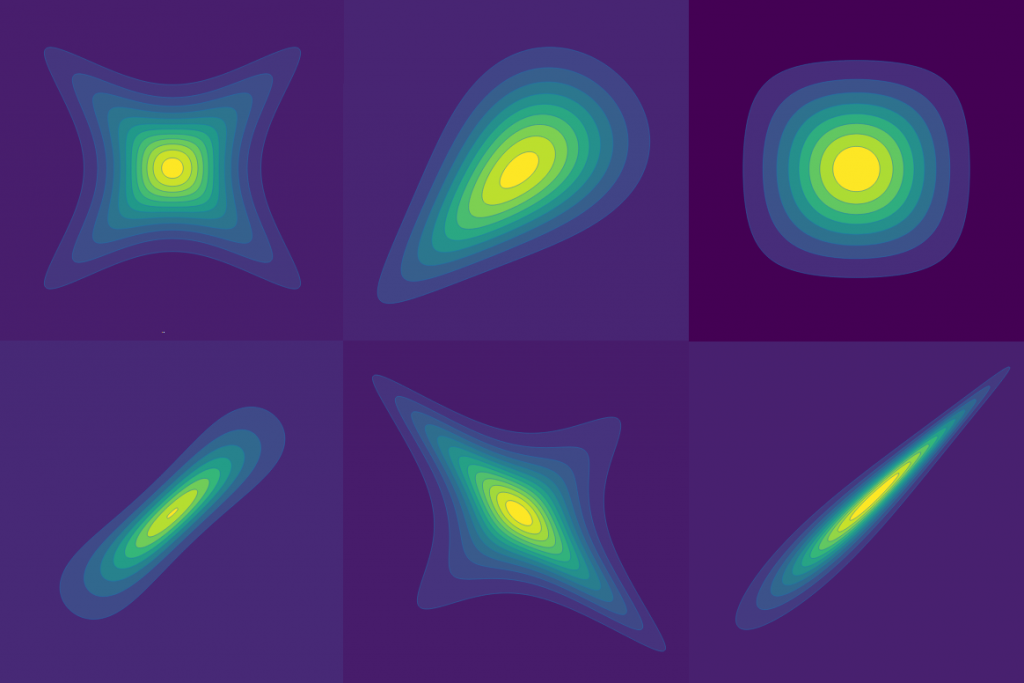

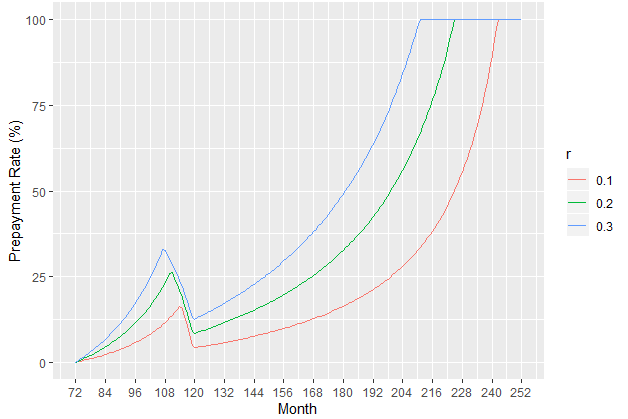

Finance The Mathematics of VaRA mathematical derivation of the Portfolio VaR highlighting the assumptions taken at each step Visit Article Common Questions about the Normal DistributionIncludes explanations of the z-scores, the confidence intervals and levels and the 68-95-99.7 rule Visit Article 3D & Contour Plots of the Bivariate Normal DistributionAn analysis of the structure of the contours and the conditional distributions Visit Article Loan PrepaymentsHow does an increase in the loan repayments affect the banks' future interest income and assets? Visit Article Different Correlation Structures in CopulasComparisons between the Gaussian, Student t, Frank, Gumbel and Clayton copulas Visit Article Portfolio VaR in 8 StepsStep-by-step worked example of the Portfolio Value-At-Risk in Excel Visit Article Computing the Portfolio VaR using CopulasModelling the marginals and the correlation structure with a copula in order to find the VaR figure Visit Article Loan PrepaymentCalculating the Prepayment Rate, Prepayment Rate Curves, Interest Lost resulting from an increase in repayments or a decrease in the interest rates Visit Article VaR Variance-Covariance Method CalculatorAn application whose inputs are stock names and quantity, and computes the value, distribution and VaR Visit Article